Introduction to Cross-Border Vehicle Buying

The European used car market is valued at $59.12 billion in 2025 and projected to reach $76.43 billion by 2031 — a 4.37% CAGR driven in part by cross-border vehicle buying. Price differentials of 10–30% between source and destination markets create consistent arbitrage opportunities for dealers and remarketing professionals who understand the regulatory, logistical, and financial mechanics of purchasing across borders.

This guide covers:

- EU single market rules — zero-duty intra-community trade and VAT reverse charge

- UK-EU post-Brexit corridor — TCA rules of origin, duty rates, and type approval

- US-Canada USMCA corridor — regional value content thresholds and RIV compliance

- Import duties by corridor — side-by-side cost comparison on a EUR 15,000 vehicle

- VAT and tax implications — reverse charge, margin scheme, and common mistakes

- Required documentation — interactive checklists by corridor

- Transport logistics and costs — method comparison and backload pricing

- Currency and payment strategies — FX impact, hedging, and provider selection

Why Cross-Border Vehicle Buying Makes Business Sense

Poland imported 13.5 million vehicles from Germany between 2004 and 2020. That single corridor illustrates the core business case: vehicles depreciate at different rates in different markets, and fleet disposal cycles create predictable supply surges that cross-border buyers can source from.

Price differentials between Western and Eastern European markets remain the primary driver. A three-year-old fleet vehicle deregistered in Germany or the Netherlands often carries a wholesale value 15–25% below what the same vehicle commands in Poland, Romania, or the Baltics. Similar dynamics exist between the US and Canada, and between the UK and EU post-Brexit.

Beyond price, cross-border buying expands inventory access. Dealers restricted to domestic auction types may struggle with limited supply in specific segments — luxury, electric, or commercial vehicles. Platforms like OPENLANE Europe (90,000+ vehicles per year, 120,000+ buyers across 50+ countries) and Autorola (200,000 vehicles per year, 70,000 active dealers) aggregate cross-border inventory at scale.

EU Single Market Rules

Zero Duty and Free Movement

Vehicles traded between EU member states move without customs duty under the principle of free movement of goods. A dealer in Poland buying from a German auction pays no import duty, files no customs declaration, and faces no border inspections. This applies to all vehicle types — passenger cars, LCVs, trucks, and motorcycles — regardless of original manufacturing origin.

The absence of customs formalities does not mean the absence of compliance requirements. The vehicle must have a valid Certificate of Conformity (CoC) or national type approval for registration in the destination country. Deregistration in the origin country and re-registration in the destination country follow national procedures that vary by member state.

VAT Reverse Charge for B2B

For B2B transactions between VAT-registered businesses in different EU member states, the VAT reverse charge mechanism applies. The seller invoices without VAT (0% intra-community supply), and the buyer self-assesses VAT at the destination country’s rate. This prevents double taxation and eliminates the need for sellers to register for VAT in every country they sell into.

Requirements for a valid reverse charge:

- Both parties hold valid VAT identification numbers

- The seller’s invoice includes both VAT-IDs and references the intra-community supply exemption

- A CMR consignment note or equivalent transport document proves the vehicle physically left the origin country

- The buyer’s VAT-ID validates through the EU VIES system

- The buyer declares the intra-community acquisition on their domestic VAT return

Platforms like CarOnSale and OPENLANE Europe facilitate these transactions by verifying buyer and seller VAT-IDs during onboarding. However, the compliance responsibility remains with the buyer and seller — not the platform.

UK-EU Post-Brexit Corridor

Since January 2021, the UK-EU Trade and Cooperation Agreement (TCA) governs vehicle trade between the UK and EU. Vehicles no longer move freely — customs declarations, rules of origin checks, and potential duty payments now apply in both directions.

Rules of Origin and Duty Rates

The TCA provides 0% duty on vehicles that meet rules of origin requirements. For internal combustion vehicles, 55% or more of the vehicle’s value must originate in the UK or EU. For electric vehicles, a transitional threshold of 45% applies through 2026, tightening to 55% from 2027.

Vehicles that do not meet these thresholds attract the standard Most Favoured Nation (MFN) duty rate of 10%. This is where many cross-border buyers encounter unexpected costs: a Japanese-manufactured car registered and driven in the UK for five years is still a Japanese car for rules of origin purposes. Re-exporting it to the EU triggers the full 10% duty.

| Scenario | Duty Rate | Key Requirement | Common Pitfall |

|---|---|---|---|

| UK-manufactured car to EU | 0% | Prove 55%+ UK/EU content | Failing to provide origin declaration |

| Japanese car re-exported UK to EU | 10% | Customs declaration + duty payment | Assuming TCA 0% applies to all UK-registered vehicles |

| EU car imported to UK | 0% | EU origin + EORI number | Not registering for UK EORI before shipment |

| Used car UK to EU (non-TCA eligible) | 10% | Full customs procedure | Underestimating documentation burden |

Type Approval: IVA and MSVA

Vehicles imported into the UK from the EU (or vice versa) require type approval in the destination market. In the UK, this means Individual Vehicle Approval (IVA) or, for vehicles over 10 years old, the Motorcycle Single Vehicle Approval (MSVA) scheme equivalent. EU-bound vehicles from the UK need national type approval in the destination member state or a valid EU Certificate of Conformity.

BCA Marketplace remains the dominant platform for UK-EU cross-border wholesale, handling vehicles in both directions. Buyers sourcing through BCA should factor type approval costs and timelines into their landed cost calculation.

US-Canada USMCA Corridor

USMCA Rules and the 75% Threshold

The United States-Mexico-Canada Agreement (USMCA) provides 0% duty on vehicles with 75% or more regional value content — meaning 75% of the vehicle’s value originates in North America. Most vehicles manufactured in the US, Canada, or Mexico meet this threshold. Vehicles that fall below it face the standard MFN duty rate: 6.1% in Canada, 2.5% in the US.

The 25-year rule in the US exempts vehicles 25 years or older from DOT and EPA compliance requirements (but not from the 2.5% duty). Canada applies a similar 15-year rule, exempting older vehicles from the Registrar of Imported Vehicles (RIV) inspection process.

Importing US Vehicles into Canada

The US-to-Canada corridor is one of the highest-volume cross-border vehicle trade routes in North America. Canadian dealers source from US auctions to access broader inventory and, when exchange rates are favorable, lower USD-denominated prices. The process involves six sequential steps.

Verify USMCA eligibility

Confirm the vehicle meets the 75% regional value content threshold for 0% duty. Most US-, Canadian-, and Mexican-manufactured vehicles qualify. Check the VIN country-of-origin code and manufacturer documentation.

Obtain export documentation

Secure the US Certificate of Title and bill of sale from the auction platform. Ensure the title is clear of liens. For vehicles purchased at auction, the auction bill of sale serves as proof of purchase price for customs valuation.

Clear Canadian customs

File a customs declaration at the Canadian border or through a licensed customs broker. Pay applicable duty (0% if USMCA-eligible, 6.1% if not) plus GST/HST on the customs value (purchase price + transport costs).

Complete RIV registration

Register the vehicle with the Registrar of Imported Vehicles within 45 days of import. The RIV fee is $295–325 CAD plus GST. RIV issues a compliance label required for provincial registration.

Pass federal safety inspection

Take the vehicle to a Transport Canada-authorized inspection facility for a Canadian Motor Vehicle Safety Standards (CMVSS) compliance check. Recalls must be completed before the vehicle passes.

Obtain provincial registration

Complete the provincial safety inspection (requirements vary by province) and register the vehicle with the provincial licensing authority. The RIV compliance label and federal inspection certificate are prerequisites.

Import Duties by Corridor

Import duty is the single line item that can eliminate a cross-border price advantage. The table below compares duty rates across the six corridors relevant to B2B auction buyers, calculated on a EUR 15,000 vehicle (or local currency equivalent).

| Corridor | Duty Rate | Conditions | Cost on EUR 15,000 Vehicle |

|---|---|---|---|

| DE → PL (intra-EU) | 0% | EU free movement | EUR 0 |

| UK → DE (TCA eligible) | 0% | Origin declaration required | EUR 0 |

| UK → DE (non-TCA) | 10% | Full customs procedure | EUR 1,500 |

| US → CA (USMCA) | 0% | 75% regional value content | CAD 0 |

| US → CA (non-USMCA) | 6.1% | Standard MFN rate | CAD 915 |

| JP → US | 2.5% | Standard MFN rate | USD 375 |

The EUR 1,500 duty on a non-TCA-eligible UK-to-EU vehicle represents a 10% cost that directly erodes the cross-border price advantage. Use the Landed Cost Calculator to model the full acquisition cost — hammer price plus duty, VAT, transport, and fees — before placing a bid. For a detailed breakdown of every cost layer — customs duty, transport, homologation, insurance, and registration taxes — with three real-world corridor examples, see the Vehicle Import Costs Breakdown.

VAT and Tax Implications

Intra-EU B2B Reverse Charge

EU VAT rates range from 17% (Luxembourg) to 27% (Hungary), with major markets falling between: Germany 19%, France 20%, Netherlands 21%, Poland 23%. On a EUR 15,000 vehicle, the VAT difference between buying in Luxembourg versus Hungary is EUR 1,500 — a significant cost variable.

For B2B cross-border transactions within the EU, the reverse charge mechanism means the buyer self-assesses VAT at the destination country’s rate. The seller issues a 0% invoice, and the buyer declares and simultaneously deducts the VAT on their return — resulting in a net-zero cash impact for VAT-registered dealers.

Margin Scheme for Used Vehicles

Dealers operating under the VAT margin scheme pay VAT only on the profit margin, not the full sale price. When buying cross-border under the margin scheme, the vehicle’s VAT status travels with it. A margin-scheme vehicle purchased from a German dealer can be resold under the margin scheme in Poland — but only if the purchase invoice clearly states the margin scheme applies.

Common VAT Mistakes

- Failing to declare the intra-community acquisition on the destination-country VAT return

- Not validating the seller’s VAT-ID through VIES before purchase

- Applying the reverse charge to B2C transactions (it applies to B2B only)

- Missing the CMR or transport proof, which invalidates the zero-rate supply

- Confusing margin-scheme vehicles with standard-VAT vehicles

For a complete breakdown of reverse charge procedures, margin scheme rules, country-by-country VAT rates, registration taxes, and documentation requirements, see the EU VAT Rules for Vehicle Purchases deep dive.

Required Documentation by Corridor

Documentation requirements vary significantly by corridor and determine whether a vehicle clears customs, qualifies for duty exemptions, and registers in the destination country. Missing a single document can delay the process by weeks and add storage or demurrage costs. Assemble the complete documentation pack before the vehicle ships.

Intra-EU Cross-Border Documents

0 of 7 completedUK-EU Post-Brexit Documents

0 of 8 completedFor a printable version with additional corridor-specific requirements, see the Cross-Border Documents Checklist.

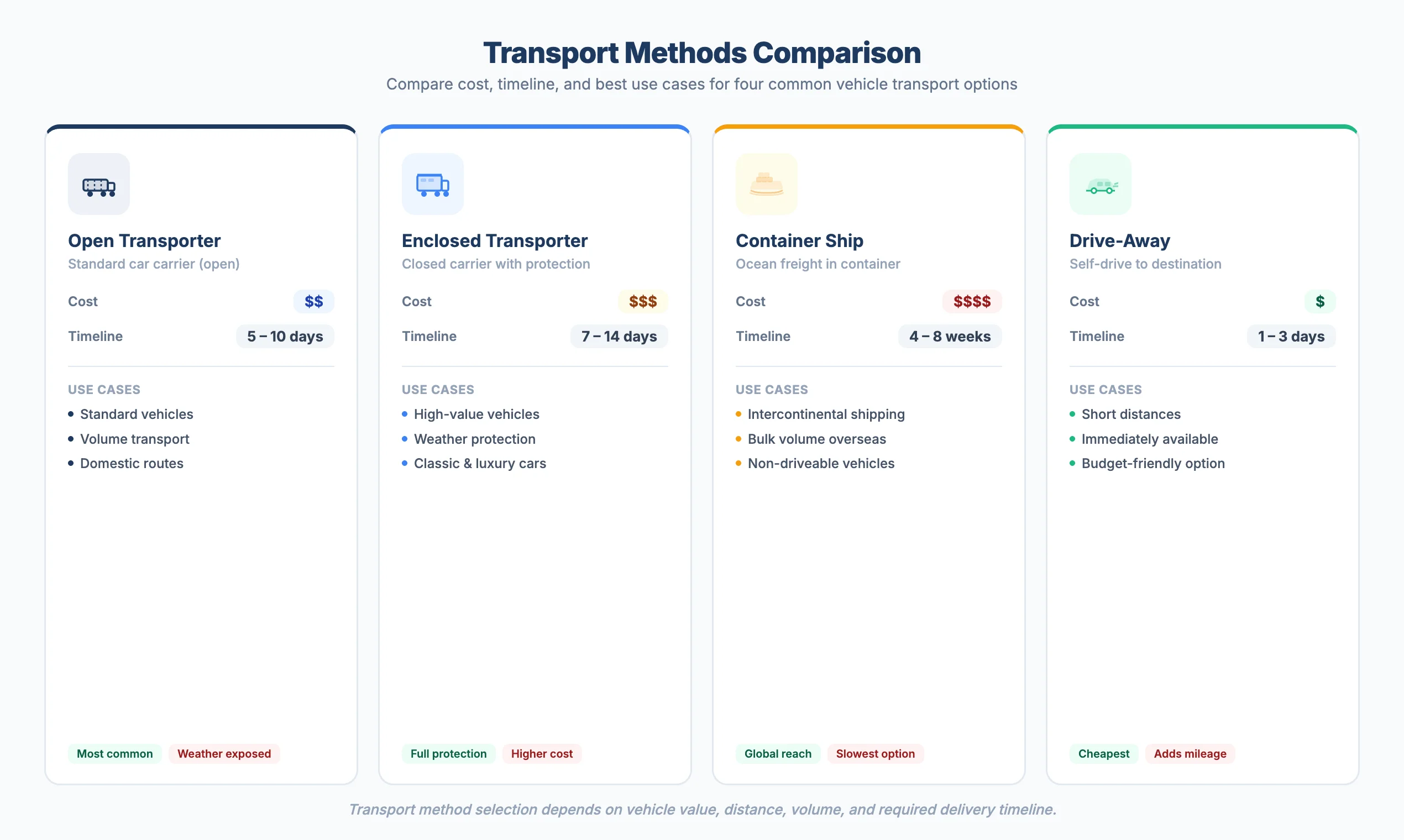

Transport Logistics and Costs

Transport cost is the second-largest variable in a cross-border landed cost calculation, after duty and VAT. The method you choose depends on distance, vehicle value, volume, and timeline.

| Transport Method | Typical Cost (Europe) | Transit Time | Best For |

|---|---|---|---|

| Open car transporter | EUR 300–800 | 2–5 days | Standard vehicles, short-medium distance |

| Enclosed transporter | EUR 600–1,500 | 2–5 days | Premium/luxury vehicles, weather protection |

| Container (RoRo) | EUR 800–2,500 | 1–4 weeks | Intercontinental, multiple vehicles |

| Drive-away service | EUR 200–600 | 1–3 days | Single vehicles, short distance |

Transport method selection depends on vehicle value, distance, volume, and required delivery timeline.

Transport method selection depends on vehicle value, distance, volume, and required delivery timeline.

Open car transporters handle the majority of European cross-border vehicle moves. Costs scale with distance: a Germany-to-Poland move (500–800 km) runs EUR 300–500, while Germany-to-Spain (1,800+ km) can reach EUR 700–800. Enclosed transport adds 50–100% to the cost but protects against road debris and weather damage during transit.

For intercontinental moves (UK-to-EU post-Brexit, US-to-Canada), Roll-on/Roll-off (RoRo) shipping is the standard method. Container shipping is an alternative for higher-value vehicles or when consolidating multiple units. Transit times extend to one to four weeks depending on port schedules and customs clearance.

Currency and Payment Considerations

FX Impact on Margins

Currency conversion costs of 1.5–3% are typical when paying for cross-border vehicles through standard bank wire transfers. On a EUR 20,000 vehicle, that translates to EUR 300–600 in FX costs — enough to erode a thin margin or turn a profitable unit into a loss.

Exchange rate volatility adds a second layer of risk. A 2% swing in EUR/GBP or USD/CAD between the time you win a bid and the time you settle payment can shift your landed cost by hundreds of euros per vehicle. For volume buyers moving 10+ units per month, unmanaged FX exposure compounds rapidly.

Hedging and Payment Strategies

- Multi-currency accounts — Hold balances in EUR, GBP, USD, and CAD to avoid conversion on every transaction

- Forward contracts — Lock in an exchange rate for future payments, eliminating volatility risk on committed purchases

- Payment timing — Settle invoices when the rate is favorable rather than on the auction platform’s default settlement date (where permitted)

- Dedicated FX providers — Specialist currency providers typically offer rates 1–2% tighter than standard bank wires

- 2% FX buffer — Build a 2% currency buffer into every cross-border max bid to absorb adverse rate movements

Conclusion and Next Steps

Cross-border vehicle buying is a margin game. The price differential between markets creates the opportunity, but duty, VAT, transport, currency conversion, and documentation costs determine whether that opportunity converts into profit.

The key decision points are: Does the vehicle qualify for 0% duty under EU free movement, TCA rules of origin, or USMCA regional value content? Is the VAT reverse charge properly structured? Have you accounted for transport costs and FX spread in your maximum bid?

Before bidding on any cross-border vehicle, model the full landed cost using the Landed Cost Calculator. Factor in all auction fees — buyer fees, seller fees, and platform charges — alongside duty, VAT, transport, and FX costs. If the number leaves margin, bid. If it does not, move on.

Frequently Asked Questions

Do I pay customs duty when buying a vehicle from another EU country?

No. Vehicles traded between EU member states move under the principle of free movement of goods with zero customs duty. There is no customs declaration or border inspection for intra-EU vehicle trade. However, VAT obligations still apply — B2B buyers self-assess VAT in their destination country under the reverse charge mechanism.

What is the VAT reverse charge for cross-border vehicle purchases?

The VAT reverse charge is a mechanism for B2B intra-EU transactions where the seller invoices at 0% VAT (intra-community supply) and the buyer self-assesses VAT at the destination country’s rate on their domestic VAT return. Both parties must hold valid VAT-IDs verified through the EU VIES system. The buyer declares the acquisition and simultaneously deducts the input VAT, resulting in a net-zero cash impact for VAT-registered businesses.

Can I import any vehicle from the US into Canada?

Most vehicles can be imported, but eligibility depends on age, safety compliance, and admissibility. Vehicles must meet Canadian Motor Vehicle Safety Standards (CMVSS) and complete the RIV process ($295–325 CAD, 45-day compliance window). Vehicles 15 years or older are exempt from RIV inspection. Some vehicles are inadmissible if they have been permanently modified or do not meet emissions standards. USMCA-eligible vehicles (75% regional value content) enter at 0% duty; others attract a 6.1% MFN rate.

What documents do I need for a UK-to-EU vehicle purchase after Brexit?

UK-to-EU vehicle purchases require: an export declaration, an import declaration, an EORI number (registered before shipment), a commercial invoice with Incoterms, the vehicle title document (V5C or equivalent), and transit documents. For TCA 0% duty eligibility, you also need an origin declaration proving 55%+ UK/EU content. The destination country may require IVA-equivalent type approval and a condition report for registration.

How do I calculate the total landed cost of a cross-border vehicle?

Total landed cost equals the hammer price plus all costs required to register and resell the vehicle in the destination market: import duty (0–10% depending on corridor and origin), VAT (17–27% in the EU, recoverable for B2B), transport (EUR 300–2,500 depending on method), currency conversion (1.5–3%), documentation and compliance fees, and any platform buyer fees. Use the Landed Cost Calculator to model these variables before bidding.