Why EU VAT Rules Matter for Cross-Border Buyers

The European Commission’s 2023 VAT Gap Report estimated EUR 128 billion in uncollected VAT across the EU — a compliance gap that tax authorities are actively closing through stricter enforcement and digital reporting requirements. For dealers and remarketing professionals buying vehicles cross-border, VAT is the single largest tax variable in every transaction. Rates range from 17% in Luxembourg to 27% in Hungary, and the regime that applies — reverse charge or margin scheme — determines whether that VAT is recoverable or embedded in your cost.

This guide covers the two core VAT regimes for B2B cross-border vehicle purchases, country-specific rates and registration taxes, documentation requirements, and the most common compliance mistakes. It complements the parent cross-border buying guide, which addresses duty, transport, and currency alongside VAT. Platforms like OPENLANE Europe and Autorola facilitate tens of thousands of intra-EU transactions annually — but the VAT compliance responsibility remains with the buyer and seller, not the platform.

New vs Used Vehicle Classification

The EU draws a hard line between “new” and “used” vehicles for VAT purposes, and the classification determines which tax regime applies. Article 2(2)(b) of VAT Directive 2006/112/EC defines a “new means of transport” as a vehicle that meets either one of two criteria: supplied within six months of its first registration, OR with 6,000 km or fewer on the odometer. Only one criterion must be met.

This definition catches vehicles that many dealers would consider “used” in commercial terms. A five-month-old fleet car with 8,000 km qualifies as “new” because it meets the age criterion (under six months). A seven-month-old car with 5,000 km also qualifies as “new” because it meets the mileage criterion (under 6,000 km). A vehicle only qualifies as “used” when it exceeds both thresholds — more than six months old AND more than 6,000 km.

The classification has direct financial consequences. New vehicles are always subject to VAT in the destination country, regardless of the seller’s status or VAT registration. The margin scheme cannot apply to new vehicles. Dealers sourcing recently deregistered fleet vehicles must verify both the first registration date and the odometer reading before assuming the vehicle qualifies for margin scheme treatment.

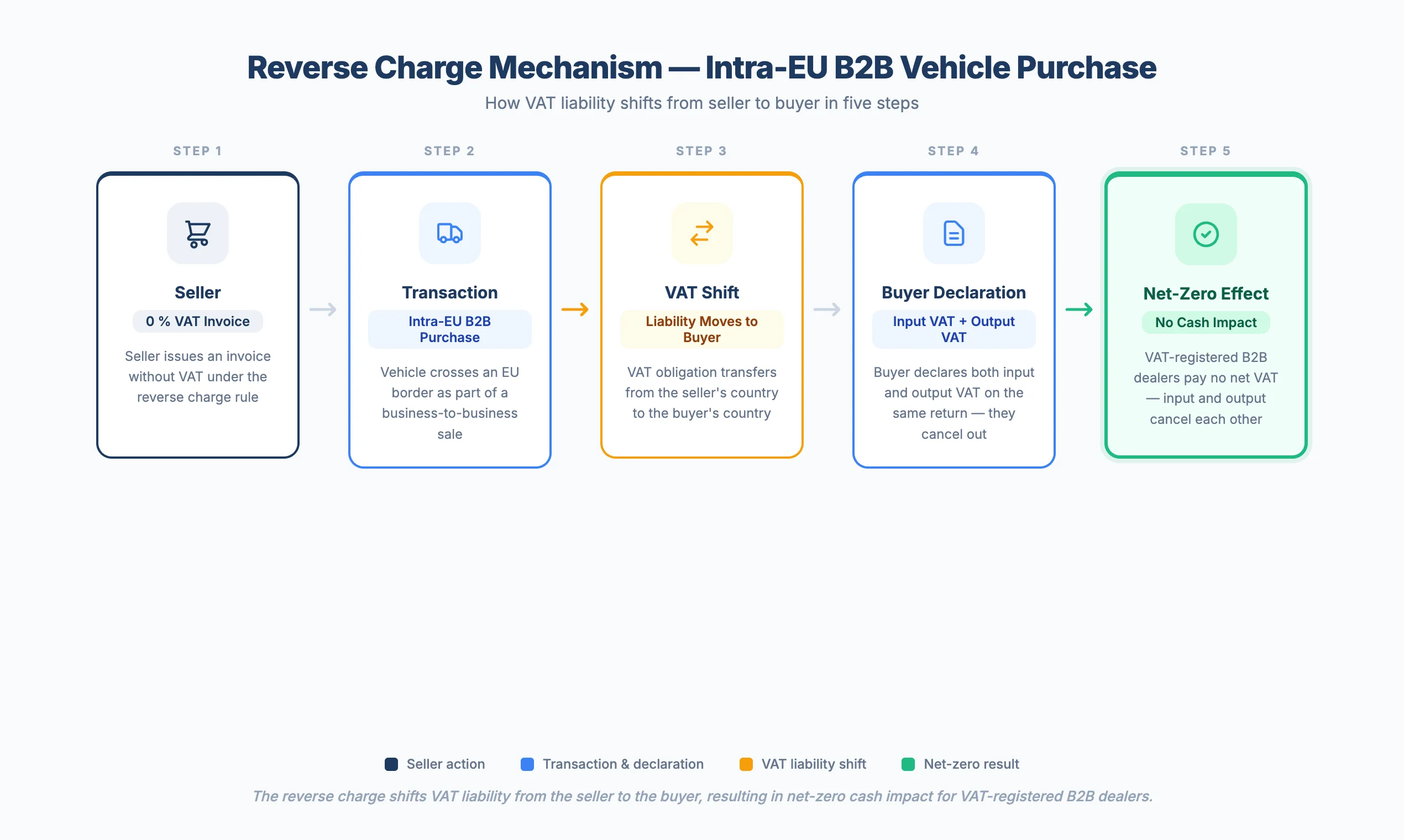

The Reverse Charge Mechanism

The reverse charge is the standard VAT treatment for B2B intra-community vehicle purchases. The core principle: the seller in the origin country invoices at 0% (intra-community supply exemption under Article 138 of the VAT Directive), and the buyer in the destination country self-assesses VAT at the local standard rate. The buyer declares the output VAT and simultaneously deducts the input VAT on the same return — resulting in a net-zero cash impact for fully VAT-registered businesses.

The reverse charge shifts VAT liability from the seller to the buyer, resulting in net-zero cash impact for VAT-registered B2B dealers.

The reverse charge shifts VAT liability from the seller to the buyer, resulting in net-zero cash impact for VAT-registered B2B dealers.

The mechanism requires five sequential steps, each with specific documentation and timing requirements.

Validate both VAT-IDs via VIES

Confirm both buyer and seller VAT identification numbers are active in the EU VIES system before the transaction proceeds. The buyer's VAT-ID country prefix must match the actual delivery destination.

Seller issues 0% invoice

The invoice must include both VAT identification numbers and reference the intra-community supply exemption (Article 138, VAT Directive). Issue the invoice by the 15th day of the month following delivery.

Arrange and document transport

A CMR consignment note or equivalent must prove the vehicle physically left the origin country. Retain at least two independent items of evidence per Article 45a of the Implementing Regulation.

Buyer declares intra-community acquisition

The buyer reports the acquisition on their domestic VAT return in the destination country, self-assessing VAT at the local standard rate.

Buyer deducts input VAT

On the same VAT return, the buyer claims the input VAT deduction. For fully VAT-registered businesses, the output and input VAT cancel out — resulting in net-zero cash impact.

Platforms like CarOnSale and OPENLANE Europe verify VAT-IDs during buyer and seller onboarding, reducing the risk of transacting with an unregistered party. However, VAT numbers can be deactivated between onboarding and the transaction date — the compliance burden rests with the parties, not the platform.

VAT Margin Scheme for Used Vehicles

The margin scheme (Articles 312–325 of the VAT Directive) offers an alternative VAT treatment for used vehicles. Under this regime, dealers pay VAT only on the profit margin — the difference between the purchase price and the resale price — rather than on the full sale price. The buyer cannot reclaim VAT on a margin-scheme purchase because the VAT is embedded in the price and not shown separately on the invoice.

The margin scheme status travels with the vehicle across borders. A margin-scheme vehicle purchased from a German dealer can be resold under the margin scheme in Poland, provided the original purchase invoice clearly states the margin scheme applies. Six rules govern the margin scheme for cross-border transactions:

- Applies only to used vehicles (more than six months old AND more than 6,000 km)

- VAT calculated on the dealer’s profit margin, not the full sale price

- Buyer cannot reclaim VAT on margin-scheme purchases

- Invoice must state “margin scheme” (e.g., “Differenzbesteuerung” in Germany) — no VAT shown separately

- Margin scheme status transfers when the vehicle is resold cross-border

- Cannot be combined with the reverse charge mechanism

The distinction between margin scheme and reverse charge has a direct impact on landed cost. Under the reverse charge, a dealer buying a EUR 15,000 vehicle self-assesses and deducts VAT — net-zero cash cost. Under the margin scheme, the embedded VAT is non-recoverable. If the selling dealer’s margin on that vehicle was EUR 2,000 and the applicable rate is 19%, EUR 380 of embedded VAT sits in the purchase price with no deduction available to the buyer.

Country-Specific VAT Rates and Registration Taxes

EU standard VAT rates range from 17% to 27%. On a EUR 15,000 vehicle purchased under the reverse charge, the VAT difference between Luxembourg (EUR 2,550) and Hungary (EUR 4,050) is EUR 1,500. For B2B buyers who self-assess and deduct, this difference washes out to net zero. For margin-scheme purchases or B2C transactions, the rate directly affects the final cost.

| Country | VAT Rate | Registration Tax | VAT on EUR 15,000 Vehicle |

|---|---|---|---|

| Luxembourg | 17% | None | EUR 2,550 |

| Germany | 19% | None | EUR 2,850 |

| Romania | 19% | None | EUR 2,850 |

| France | 20% | Minor registration fees | EUR 3,000 |

| Austria | 20% | NoVA (CO2-based) | EUR 3,000 |

| Netherlands | 21% | BPM (CO2-based, can add thousands) | EUR 3,150 |

| Belgium | 21% | BIV (registration tax) | EUR 3,150 |

| Czech Republic | 21% | None | EUR 3,150 |

| Spain | 21% | IEDMT (registration tax) | EUR 3,150 |

| Italy | 22% | IPT (provincial tax) | EUR 3,300 |

| Ireland | 23% | VRT (up to 37% of OMSP) | EUR 3,450 |

| Poland | 23% | Akcyza (3.1% / 18.6%) | EUR 3,450 |

| Portugal | 23% | ISV (engine + CO2 based) | EUR 3,450 |

| Denmark | 25% | Up to 150% of vehicle value | EUR 3,750 |

| Sweden | 25% | Annual vehicle tax only | EUR 3,750 |

| Hungary | 27% | Engine/age-based registration tax | EUR 4,050 |

Registration taxes are separate from VAT and typically non-recoverable — they apply regardless of B2B or B2C status. In Denmark, the registration tax alone can reach 150% of the vehicle’s value, making cross-border imports into Denmark prohibitively expensive for most vehicle categories. The Netherlands (BPM), Ireland (VRT at up to 37% of open market selling price), and Poland (akcyza at 3.1% for engines under 2,000 cc or 18.6% above) impose registration taxes that can exceed the VAT amount on the same vehicle.

These non-recoverable taxes must be modeled into the landed cost before calculating a maximum bid with the Break-Even Max Bid Calculator. A vehicle that appears profitable based on hammer price plus VAT may become a loss once the destination country’s registration tax is applied.

Documentation Requirements

Proper documentation is non-optional for the reverse charge. Missing a single item can cause the origin country’s tax authority to deny the 0% rate, making the seller liable for domestic VAT. Article 45a of the Implementing Regulation requires at least two independent items of evidence proving the vehicle physically left the origin country.

Assemble the complete documentation pack before the vehicle ships. Tax authorities audit intra-community supplies retrospectively, and gaps discovered months after the transaction are expensive to resolve.

Reverse Charge Documentation Checklist

0 of 9 completedCommon EU VAT Mistakes

Six errors account for the majority of VAT compliance failures in cross-border B2B vehicle transactions. Each carries financial consequences that range from delayed VAT recovery to double taxation.

| Mistake | Consequence | Prevention |

|---|---|---|

| Missing acquisition declaration | Double VAT — paid in origin, no deduction in destination | Declare intra-community acquisition on every VAT return period |

| Invalid or expired VAT-ID | Seller cannot apply 0% rate; liable for domestic VAT | Run VIES check on the day of transaction |

| Margin scheme confusion | Buyer assumes VAT is reclaimable when it is not | Verify invoice states margin scheme or standard VAT before bidding |

| Insufficient transport proof | Tax authority denies 0% rate; missing Article 45a evidence | Collect CMR plus one additional independent evidence item |

| VAT number / country mismatch | VAT-ID does not match delivery destination country | Confirm VAT-ID country prefix matches actual delivery destination |

| Treating B2C as B2B | Reverse charge applied to non-business buyer | Verify buyer's VAT registration before applying 0% rate |

The missing acquisition declaration is the most financially damaging error on this list. When a buyer fails to report the intra-community acquisition on their destination-country VAT return, the origin country’s tax authority may assess the seller for domestic VAT (which the seller then passes to the buyer). Meanwhile, the destination country’s authority receives no declaration to trigger the input VAT deduction. The result: VAT paid in the origin country with no corresponding deduction in the destination country.

Frequently Asked Questions

Do I pay VAT when buying a vehicle from another EU country as a B2B dealer?

Yes, but under the reverse charge mechanism you self-assess VAT at the destination country’s rate and deduct it simultaneously on the same VAT return. For fully VAT-registered dealers, the net cash impact is zero. The seller invoices at 0% as an intra-community supply, provided both parties hold valid VIES-verified VAT identification numbers.

What is the difference between the reverse charge and the margin scheme?

The reverse charge is the standard B2B intra-community treatment: the buyer self-assesses VAT at the destination rate and deducts it on the same return, resulting in net-zero cash impact. The margin scheme applies to used vehicles where the seller pays VAT only on the profit margin — the buyer cannot reclaim this embedded VAT. The two regimes are mutually exclusive. Check the invoice to confirm which applies before bidding.

How does the EU define a “new” vehicle for VAT purposes?

A vehicle qualifies as “new” under Article 2(2)(b) of VAT Directive 2006/112/EC if it is less than six months old OR has 6,000 km or fewer on the odometer. Only one condition must be met. New vehicles are always subject to destination-country VAT regardless of the seller’s status, and the margin scheme cannot apply to them.

Which EU countries charge registration taxes beyond VAT?

Denmark imposes the highest registration tax in the EU — up to 150% of the vehicle’s value. The Netherlands charges BPM (CO2-based, potentially thousands of euros). Ireland applies VRT at up to 37% of the open market selling price. Poland charges akcyza at 3.1% for engines under 2,000 cc and 18.6% for larger engines. Austria (NoVA), Spain (IEDMT), and Portugal (ISV) also impose registration taxes. All are non-recoverable. Use the Landed Cost Calculator to model these costs before bidding.

What happens if the buyer’s VAT number is invalid at the time of sale?

The seller cannot apply the 0% intra-community supply exemption and becomes liable for VAT at the origin country’s domestic rate. The buyer must then reclaim the origin-country VAT through the Directive 2008/9/EC cross-border refund process, which takes four to eight months. Validate the buyer’s VAT-ID through VIES on the transaction date to prevent this scenario.